Okay, so your old HVAC system is giving up the ghost. You know that wheezing, groaning sound? The one that makes you wonder if it’s about to spontaneously combust into a cloud of glitter and despair? Yep, that one. It’s time for a new hero to swoop in and save your comfort. But wait, the price tag! Gulp. Don't panic! Financing your new HVAC system doesn't have to be a snoozefest. In fact, we can make it kinda fun. Think of it as a treasure hunt for the best deal!

Seriously, who knew buying a giant metal box that controls your house's temperature could be so… exciting? It’s like a financial adventure, a quest for coolness (or warmth, depending on your immediate needs, you lucky duck!). And the prize? A perfectly regulated home where you can finally stop wearing a parka indoors during summer or sweating through your couch cushions in winter.

So, let's dive into the nitty-gritty of making this happen without selling a kidney. (Unless you have a spare, in which case, maybe keep that option on the table? Just kidding! Mostly.)

Your HVAC Financing Quest: The Big Picture

Before we get into the nitty-gritty, let's get our bearings. Financing a new HVAC system is basically finding a way to pay for it without emptying your entire savings account in one go. Easy peasy, right? Well, almost.

Think of it like this: you’re building your personal comfort fortress. And fortresses, my friends, require resources. We're just being smart about how we gather those resources.

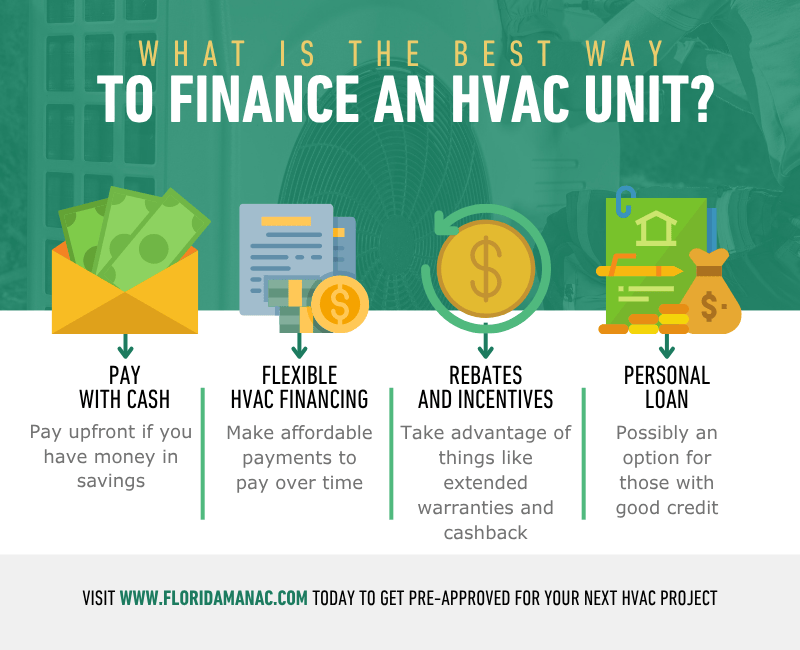

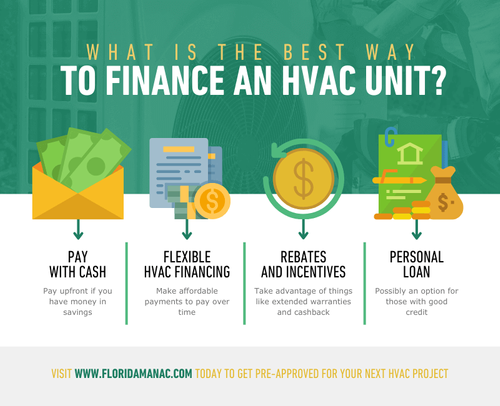

The best way to finance? It's not a one-size-fits-all answer. It's more like a buffet of options, and you get to pick the tastiest morsels. We're talking about options that are affordable, convenient, and maybe even come with a side of sweet deals.

Option 1: The "It's Just Like a New Fridge" Method - Personal Loans

Ever financed a fancy new appliance? A personal loan is kinda like that, but for your entire house's climate control. You get a lump sum of cash from a bank or credit union, and then you pay it back over time with interest.

Pros: It’s pretty straightforward. You can often get a good interest rate if your credit is in decent shape. Plus, once you’ve got the cash, you can pay for the HVAC system upfront, which sometimes gets you a discount from the installer. Booyah!

Cons: You need decent credit. If your credit score is lower than your enthusiasm for doing laundry, this might not be your golden ticket. Also, interest is, well, interest. It adds to the total cost.

Fun Fact: Did you know personal loans date back to ancient Mesopotamia? People were probably borrowing barley to fund their chariot upgrades back then. So, you're participating in a very, very old tradition! Just, you know, with less mud and more spreadsheets.

Option 2: The "Specialty Superhero" - HVAC Contractor Financing

Many HVAC companies partner with lenders to offer their own financing plans. Think of them as the friendly neighborhood superheroes of home comfort, complete with their own financial cape.

Pros: This is often super convenient. You can apply right there and then, during your installation consultation. No running around to different banks. Plus, they sometimes offer special promotional rates, like 0% interest for a certain period. Score! This can save you a bundle on interest if you can pay it off quickly.

Cons: The interest rates after the promotional period might be a bit higher than a traditional personal loan. It’s always, always, always read the fine print, even if it feels like you're deciphering ancient hieroglyphs.

Quirky Detail: Some of these plans are so slick, they’re like a ninja in the night. You’ll barely notice the payments creeping out of your bank account… until the statement arrives, of course. But in a good way! A planned way.

Option 3: The "Magic Wand" - Home Equity Loans or HELOCs

Got some equity built up in your home? Like a hidden treasure chest of cash? A home equity loan or a Home Equity Line of Credit (HELOC) can be a fantastic way to tap into it.

Pros: Interest rates are often lower than personal loans because your home is the collateral. This can make a big difference in the long run. Plus, the interest you pay might even be tax-deductible. Talk about a win-win!

Cons: This is where the “adventure” part gets a little more serious. You’re using your home as collateral. If you can't make the payments, you could risk losing your house. So, make sure you’re super confident in your ability to repay. It’s like walking a tightrope – exciting, but you need to be steady!

Funny Thought: Imagine telling your friends you financed your new AC with your "house's piggy bank." Sounds pretty darn cool, right?

Option 4: The "Government Good Guy" - PACE Financing

PACE stands for Property Assessed Clean Energy. It’s a government-backed program that allows homeowners to finance energy-efficient upgrades (like a super-duper HVAC system!) through their property taxes.

Pros: Often has low interest rates and you don’t typically need a credit check! The payments are spread out over a long period, usually up to 20 years, and they appear on your property tax bill. It's like a financial ghost, quietly working in the background.

Cons: It’s not available everywhere. You’ll need to check if your local government offers it. And since it’s tied to your property taxes, it can impact the sale of your home down the line. Plus, it’s a lien on your property, similar to a mortgage.

Intriguing Fact: PACE financing was designed to encourage energy efficiency. So, not only are you getting a comfy home, but you're also giving Mother Earth a little pat on the back. High five!

Option 5: The "Patience is a Virtue" - Good Old Savings

Okay, okay, I know this isn't technically "financing" in the loan sense, but hear me out! If you have the savings, or can save up for a bit, paying cash can be the absolute best way.

Pros: Zero interest! You own your system outright from day one. This means your monthly bills are solely for your cozy climate, not for paying off debt. Plus, it gives you serious bragging rights.

Cons: You have to wait until you have the money. And let’s be real, nobody wants to wait for cool air when it's 90 degrees outside. It requires discipline, like resisting the urge to eat the entire tub of ice cream in one sitting. (Though, a new HVAC system does make ice cream consumption much more enjoyable.)

Playful Proverb: "A penny saved is a penny earned… and a much cooler summer." Or something like that. The point is, saving is awesome!

Making Your Decision: The Grand Finale

So, which option is the best? It depends on your personal situation. Think about:

- Your Credit Score: This is a biggie. Good credit opens more doors.

- Your Savings: How much wiggle room do you have?

- Your Home Equity: Is your house acting as a secret financial vault?

- Your Risk Tolerance: Are you okay with using your home as collateral?

- The Installer's Offers: Always ask about their financing specials!

Don't be afraid to shop around. Get quotes from different HVAC companies and explore various financing options. It’s like comparing different flavors of ice cream – you want the best one for your palate (and your wallet!).

Ultimately, financing a new HVAC system is an investment in your home and your happiness. So, have fun with it! Be informed, be savvy, and get ready to enjoy perfectly regulated air for years to come. You've got this!