Remember Sarah and Tom? They were young, super excited, and just bought their first fixer-upper. Picture this: they’re standing in their dusty living room, surrounded by boxes, a faint smell of old carpet in the air, and Tom, ever the optimist, says, “Honey, this is it! Our little slice of heaven!” Sarah, meanwhile, is eyeing a suspiciously water-stained ceiling and muttering something about calling the landlord… I mean, the contractor.

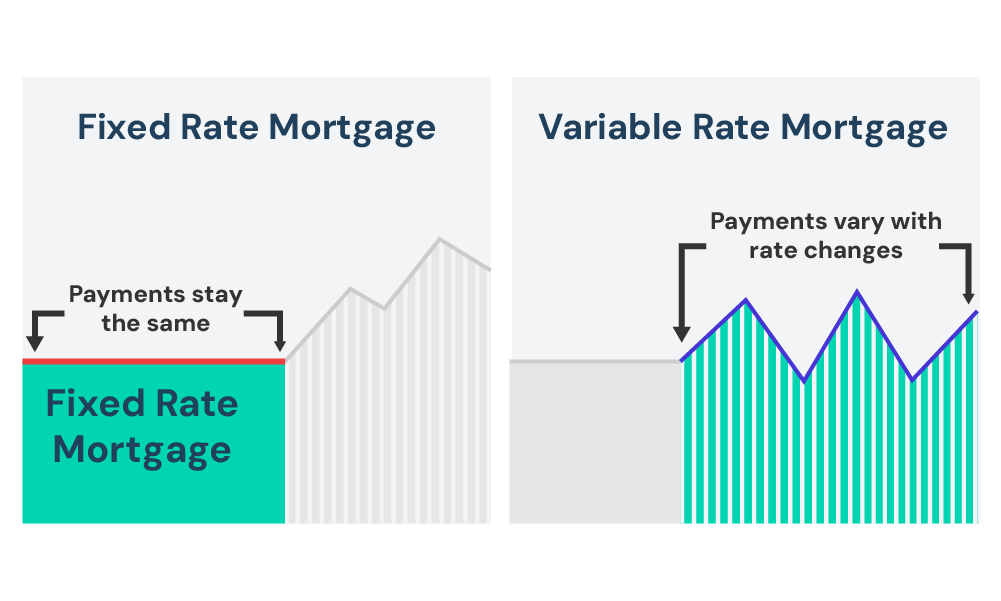

The dream was real, but then came the reality. The reality of bills. And one of the biggest, most looming bills was that mortgage payment. They’d sat down with the bank, signed a stack of papers thicker than Sarah’s favorite novel, and now, every month, a chunk of their hard-earned cash was going to be whisked away. The kicker? They’d opted for a fixed-rate mortgage. And for a while, they weren’t entirely sure if that was a good thing or… well, just a thing.

This is where we dive into the glorious, sometimes bewildering, world of your monthly fixed-rate mortgage payment. It’s that magical (or sometimes mundane) number that pops up on your bank statement like clockwork. And understanding it is, dare I say, as crucial as knowing where to find the studs in your wall when you’re hanging that new flat-screen TV. Trust me on this one.

So, What Exactly Is This Monthly Fixed-Rate Thingy?

Let’s break it down, shall we? Imagine you’re borrowing a giant pile of money to buy your house. Obvious, right? That money doesn’t just magically appear. You’ve got to pay it back, with a little extra for the bank’s troubles. That extra is called interest. Now, there are different ways to structure that repayment, and one popular method is the fixed-rate mortgage.

The “fixed” part is the key here. It means that for the entire duration of your loan – we’re talking 15, 20, even 30 years – your interest rate stays the same. No surprises. No spooky hikes in your monthly bill because the economy decided to throw a tantrum. Your payment for the principal (the actual loan amount) and the interest is set in stone from day one.

Think of it like ordering your favorite pizza with all your usual toppings. You know exactly what you’re going to get, and the price is always the same. You don’t have to worry about the cost of pepperoni suddenly skyrocketing next month, or the cheese market crashing. It’s just… consistent. And in the world of homeownership, where there are already enough curveballs to make a seasoned pitcher sweat, consistency is gold. Pure, unadulterated, gold.

Why is “Fixed” Such a Big Deal?

Well, let’s contrast it with its flashy cousin, the adjustable-rate mortgage (ARM). With an ARM, your interest rate can go up or down over time, usually tied to some economic indicator. It might start with a lower, super-attractive introductory rate (the “teaser rate,” as some like to call it – sounds a bit shady, doesn’t it?), but then, BAM! That rate could start climbing, making your monthly payment significantly higher.

And when that happens, your budget might do a little jig it didn’t sign up for. Suddenly, that dream home feels a little less… dreamy. Sarah and Tom, bless their hearts, had heard horror stories from friends who’d gone the ARM route and watched their payments balloon. So, they played it safe, and for them, safe felt really good.

A fixed-rate mortgage offers that sweet, sweet predictability. You know, month in and month out, exactly how much you need to set aside. This makes budgeting infinitely easier. You can plan for vacations, kids’ college funds, or even just that fancy new coffee maker you’ve been eyeing, with a much clearer picture of your financial landscape. No more nervously checking the news for interest rate hikes, wondering if your bank account is about to take a hit. Phew!

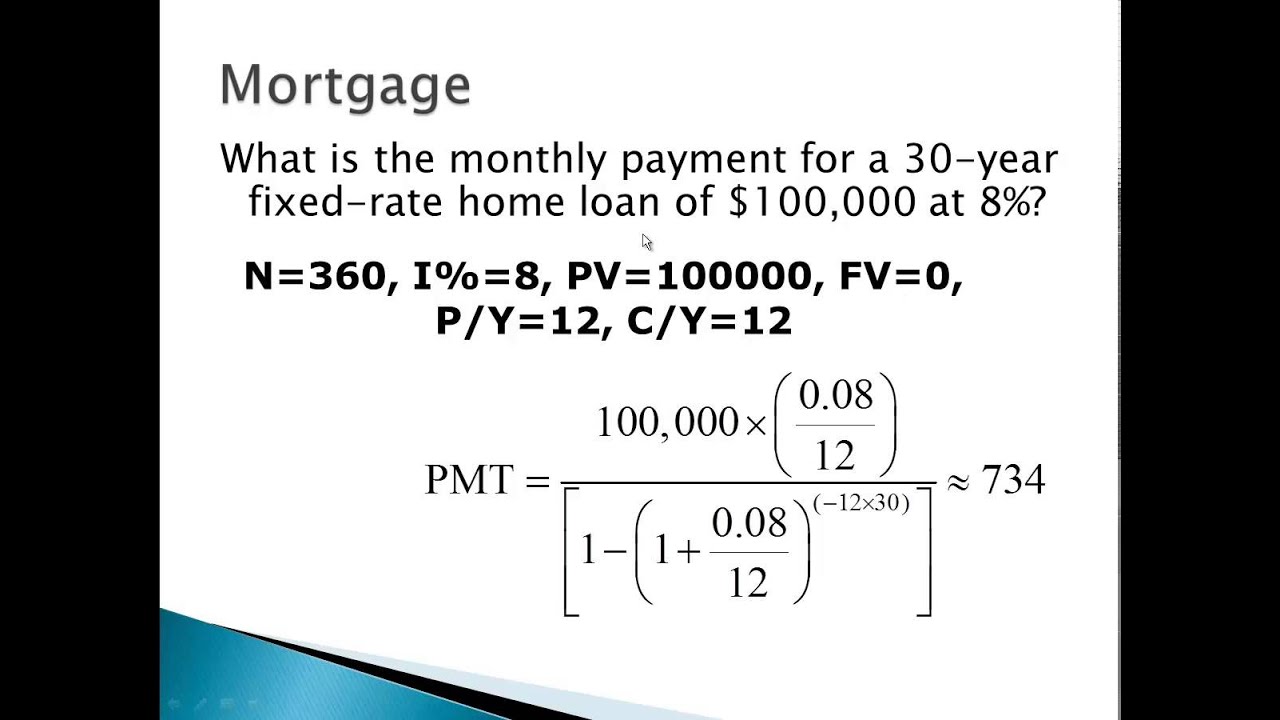

Deconstructing Your Monthly Payment: It’s Not Just Principal and Interest

Ah, the actual payment. When you see that number, it’s tempting to think it’s just the loan amount divided by the number of months, plus some interest. But, my friends, that’s usually just the tip of the iceberg. For most people, their monthly mortgage payment is actually a little package deal, often referred to as PITI.

Now, don’t panic at the acronym. It’s not some scary government tax. PITI stands for:

- Principal: This is the actual money you borrowed to buy the house. A portion of your payment goes towards reducing this balance.

- Interest: This is the fee the lender charges for letting you borrow their money. As we discussed, in a fixed-rate mortgage, this percentage stays the same.

- Taxes: Yes, property taxes. Your local government loves them. And your mortgage lender, to make sure you don’t skip out on paying them (which could jeopardize their loan!), often collects a portion of your estimated annual property taxes with each monthly payment.

- Insurance: This usually includes your homeowner’s insurance (to protect against fire, theft, natural disasters, etc.) and sometimes Private Mortgage Insurance (PMI) if your down payment was less than 20%.

So, that monthly bill you’re paying? It’s doing a lot more than just paying off your loan. It’s also essentially a savings account for your property taxes and insurance premiums. Your lender holds onto that money and pays those bills for you when they come due. It’s a convenience, to be sure, but it also means that your PITI payment will change if your property taxes go up or down, or if your insurance premiums are adjusted.

This is a crucial point. While the principal and interest portion of your fixed-rate mortgage payment remains constant, your total monthly payment (PITI) can still fluctuate. It’s like buying a subscription box. The price of the core items might be fixed, but if the shipping costs or a new regulatory fee gets added, the final bill might be slightly different. Just something to keep in mind so you don’t have a mini-meltdown when your statement arrives!

The Amortization Schedule: Your Financial Roadmap

So, how does that principal and interest payment actually work over the years? Enter the amortization schedule. This is, quite frankly, one of the most fascinating (and slightly depressing, if you’re feeling dramatic) documents you’ll ever see related to your mortgage. It’s a detailed breakdown showing, for every single payment you make, how much is going towards interest and how much is going towards principal.

Here’s the funny thing about amortization: in the early years of your loan, the majority of your payment is going towards… you guessed it… interest! It feels a bit like you’re paying a hefty membership fee just to have the loan. Only a small chunk is chipping away at the actual debt. It’s like trying to empty a swimming pool with a teaspoon at the beginning.

But don’t despair! As the years go by, the tables slowly turn. The amount of interest you pay decreases with each payment, and the amount going towards your principal balance increases. By the time you reach the end of your loan term, almost your entire payment is dedicated to paying down that principal. It’s a long game, for sure, but the balance eventually tips in your favor. You just have to keep at it, like a determined ant carrying a crumb twice its size.

You can usually find your amortization schedule from your lender. It’s a great tool for visualizing your progress and understanding how your payments are working for you. It’s also a handy way to see how much equity (the difference between your home’s value and what you owe on the mortgage) you’re building over time. Pretty neat, huh?

The Beauty of Predictability: When the World Gets Crazy

Let’s circle back to Sarah and Tom. They’re now a few years into their mortgage. The dusty living room has been transformed into a cozy haven, and the water stains? Well, let’s just say they’re a distant, humorous memory. What they haven’t forgotten is the peace of mind their fixed-rate mortgage provides.

![[FREE] The monthly payment on a loan may be calculated by the following](https://media.brainly.com/image/rs:fill/w:3840/q:75/plain/https://us-static.z-dn.net/files/d6f/74a6c002c722bfb27fabf7a819da6e60.png)

They’ve seen friends panic as interest rates jumped, forcing them to cut back on other expenses. They’ve heard about people struggling to make their payments because of unexpected economic shifts. But Sarah and Tom? Their mortgage payment has remained the same, an island of financial stability in a sometimes turbulent sea.

This is the real power of a fixed-rate mortgage. It’s not just about the number itself; it’s about the certainty it brings. It allows you to plan for the future with confidence. It insulates you from the unpredictable swings of the market. It lets you sleep at night knowing that a fundamental part of your biggest financial commitment won’t suddenly change overnight.

Think about it. In life, so much is out of our control. The weather, traffic, the latest fashion trends. But your principal and interest payment on a fixed-rate mortgage? That’s something you can control, in the sense that you know exactly what it will be. This is a huge psychological comfort, especially when you’re juggling all the other demands of modern life.

Are There Any Downsides to a Fixed Rate?

Okay, okay, no good thing is perfect, right? And while fixed-rate mortgages are fantastic for many, there are a couple of things to consider. The most common point of comparison is that introductory rates on ARMs are often lower. So, in the very beginning, your fixed-rate payment might be a tad higher than an ARM’s initial payment.

However, this is where you have to look at the long game. That initial difference might be small, but the potential for an ARM’s rate to climb significantly later on is a much bigger risk. It’s like choosing between a slightly higher upfront cost for a truly reliable car versus a cheaper car that might need constant, expensive repairs down the road. Most people would opt for the reliable one, wouldn’t they?

Another scenario where a fixed rate might not be the absolute best is if you plan to sell your home relatively quickly. If you’re only going to be in the house for, say, two to five years, and interest rates are very low, an ARM might offer some initial savings. But even then, the risk of rates rising before you sell is always there. And selling a house also comes with its own set of costs and complexities, so trying to game the mortgage rate might not be worth the headache.

Ultimately, for the vast majority of homeowners, especially those planning to stay put for a while, the stability and security of a fixed-rate mortgage are well worth any minor initial difference in payment. It’s an investment in peace of mind, and in the world of homeownership, that’s priceless.

In Conclusion: Your Monthly Payment is Your Homeownership Anchor

So, there you have it. Your monthly fixed-rate mortgage payment. It’s more than just a number on a statement; it’s a carefully calculated promise, a pact between you and your lender, designed to provide clarity and security. It’s the bedrock upon which you build your home and your financial future.

Whether you’re Sarah and Tom, just starting out and a little overwhelmed, or a seasoned homeowner looking back, understanding this core element of your finances is crucial. It empowers you to budget effectively, plan for the long term, and, most importantly, to truly enjoy the journey of homeownership without constant financial anxiety.

So, the next time you see that payment come out of your account, take a moment. Appreciate the predictability. Appreciate the journey you’re on. Because that steady, unwavering number is a testament to your hard work, your dreams, and the security of your very own home. And that, my friends, is something to be really, really happy about.

![[FREE] What’s the down payment ? Whats the amount of mortgage ? Whats](https://media.brainly.com/image/rs:fill/w:3840/q:75/plain/https://us-static.z-dn.net/files/d74/beb776c6410a445317b4090e84b636b6.jpg)